As Realtors, we have a fiduciary responsibility to provide our clients with the best advice and options to serve their financial interests. When it comes to saving them money on capital gains taxes from selling investment properties, a 1031 exchange will almost always be in their best interest. The only problem is that 1031 exchange rules are complex.

If you want to work with investors, you need to know how to explain their complexities in plain English. To make your job easier, I put together this simple 1031 exchange rules cheat sheet to help you save your clients money at tax time. There’s a lot to digest here, so if you’re in a rush, you can simply download my 1031 Exchange Rules Cheat sheet as a PDF here:

Download Your Free Branding Guide

Back to Basics: What Is a 1031 Exchange?

A 1031 exchange refers to section 1031 of the Internal Revenue Code, which allows a property to be exchanged for a “like-kind” property. The benefit of a 1031 exchange is that it defers the taxes that would normally be paid on the capital gains from the sale of a property.

While everyone would like to save money on capital gains when selling their home and buying a new one, 1031 exchanges are only allowed on investment properties. If you don’t have any investor clients yet, check out my quick start guide to building the skills investors look for in Realtors here:

9 Skills Agents Need to Work With Investors & Close 50-100 Deals a Year

How 1031 Exchanges Work + Examples

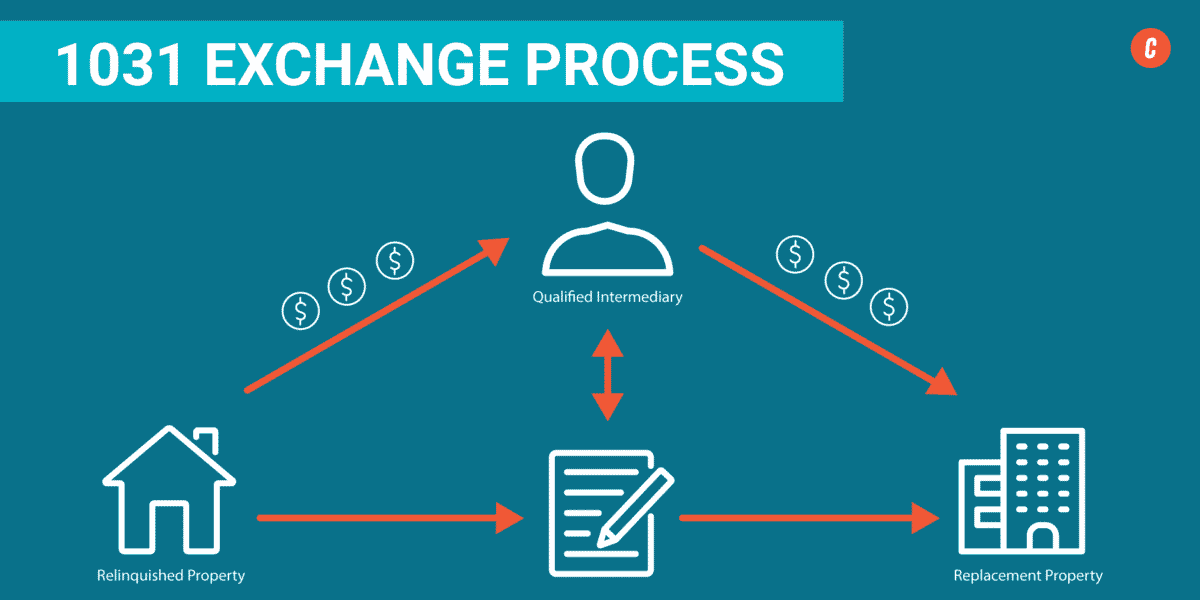

A 1031 exchange is the process where a person sells one investment property and purchases another “like-kind” property (or multiple properties) of equal or greater value than the property sold.

The first property—the one your client is selling—is known as the Relinquished Property, and the like-kind property they are purchasing is known as the Replacement Property.

The proceeds from the sale may not be received by the seller. Basically, the money cannot hit their bank account. Instead, the money from the sale of their first investment property must be transferred to a qualified intermediary (known as a QI), who will hold the funds until the replacement property is identified and purchased.

When all of the proceeds from the sale of the relinquished property are used for the purchase of the replacement property, the sale is considered an exchange and is not a taxable event. The advantage to your client is that they will not have to pay capital gains tax on the uptick in value of the property they’ve sold.

When Taxes Must Be Paid on 1031 Exchanges

Any proceeds from the sale of the relinquished property that is not used to purchase the replacement property is called “boot” and is subject to taxation.

Additionally, if the relinquished property has a mortgage loan outstanding on it, the replacement property must have equal or greater debt. If the debt on the replacement property is less than the previous debt on the relinquished property, the difference is called “Mortgage Boot” and is subject to capital gains tax.

This is important to note since many investors want to use their property sale proceeds to buy a lesser-priced property, and thus avoid having a mortgage on their newest investment. Doing so, however, will not satisfy the rule of replacing the value in a 1031 exchange.

Example of a 1031 Exchange

A client has a single-family investment property in Denver, Colorado. They want to sell their Denver property and purchase two duplexes in Chattanooga, Tennessee.

The home in Denver is valued at $600,000 and has an outstanding mortgage balance of $300,000. After the sale, they’ll need to pay the balance of the mortgage, in addition to the cost of closing the sale ($48,000), leaving them with $252,000.

Since the proceeds from the sale may not be given to the seller, they must find a qualified intermediary to hold the funds until the purchase of the replacement property or properties (in this case, the two duplexes in Chattanooga) is complete.

The qualified intermediary will complete the necessary paperwork that the title company and IRS require to ensure the transaction is completed correctly.

Once the Relinquished Property sale is complete, the seller must identify three “like-kind” replacement properties within 45 days. In this case, the seller is exchanging the single-family home in Denver that they rent out for two duplexes in Tennessee that they will use to generate income through rent and appreciation.

As such, their desired Tennessee properties qualify this as a “like-kind” transaction, eligible for a 1031 exchange.

Replace the Total Value

To avoid taxation on capital gains, 100% of the value of the Relinquished Property must be replaced by property or properties of equal or greater value. Therefore, our seller must find properties with a total value equal to or greater than $600,000.

In this example, our seller identified and contracted the two Tennessee duplexes for the combined sales price and replacement value of $640,000.

Once the properties are placed under contract, the purchase transactions must be completed within 180 days of the date of the sale of their Denver property. The seller must also use the full proceeds from the sale of their single-family home in Denver toward the purchase of the duplexes. Otherwise, any unused portion, or “Boot,” may be subject to capital gains tax.

Since the proceeds of $252,000 from the sale of the home in Denver isn’t enough to cover the combined purchase price of $640,000 for the two duplexes, the investor will need to either secure a mortgage or bring in the additional cash to make up the difference.

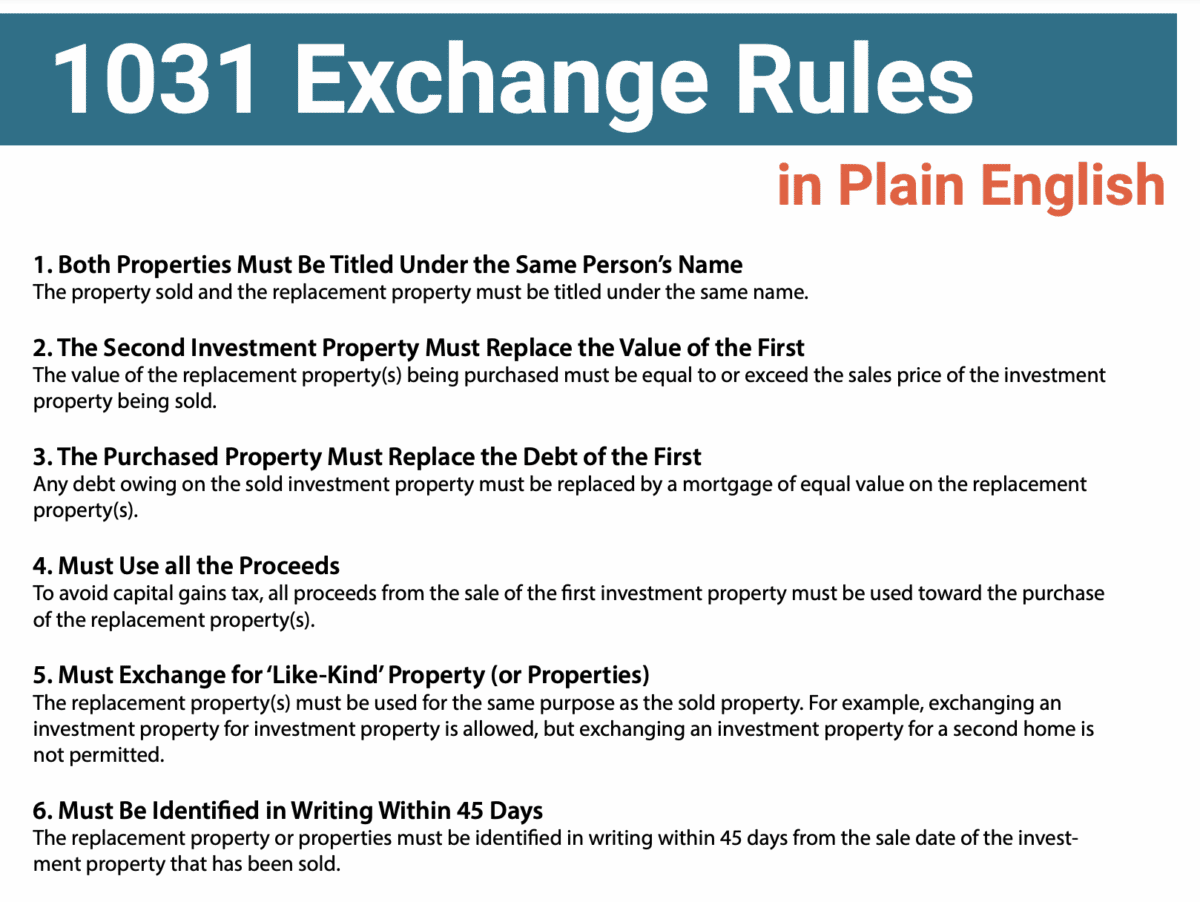

1031 Exchange Rules in Plain English

While 1031 exchange rules can get a little complicated, being able to discuss the basic rules with your clients will help you come across as a true professional. Here is a quick rundown of 1031 exchange rules:

1031 Exchange Rules in Plain English

1. Both Properties Must Be Titled Under the Same Person’s Name

The property sold and the replacement property must be titled under the same name.

2. The Second Investment Property Must Replace the Value of the First

The value of the replacement property(s) being purchased must be equal to or exceed the sales price of the investment property being sold.

3. The Purchased Property Must Replace the Debt of the First

Any debt owing on the sold investment property must be replaced by a mortgage of equal value on the replacement property(s).

4. Must Use All the Proceeds

To avoid capital gains tax, all proceeds from the sale of the first investment property must be used toward the purchase of the replacement property(s).

5. Must Exchange for ‘Like-Kind’ Property (or Properties)

The replacement property(s) must be used for the same purpose as the sold property. For example, exchanging an investment property for investment property is allowed, but exchanging an investment property for a second home is not permitted.

6. Must Be Identified in Writing Within 45 Days

The replacement property or properties must be identified in writing within 45 days from the sale date of the investment property that has been sold.

7. Must Close in 180 Days

The purchase of the replacement property or properties must be completed within 180 days from the sale date of the sold investment property. Once the new property is identified, your clients have 180 days from their first closing to close on their replacement property.

8. Must Not Have Access to the Proceeds of the Sale

The seller (or exchanger) may not have access to any of the proceeds from the sale of their investment property until the 1031 exchange process is complete.

Answers to Common 1031 Exchange Rule Questions

No article can answer every question about 1031 exchanges. However, here is a short list of the most common questions your clients may have and how to answer them.

What Qualifies as a ‘Like-Kind’ Property for a 1031 Exchange?

One of the most important and confusing conditions of a 1031 exchange is the “like-kind” property rule. This states that the Replacement Property must be “like-kind” to the Relinquished Property.

The Internal Revenue Code defines a “like-kind” property as any real estate within the U.S. that is held for investment, trade, or business purposes. A “like-kind” property cannot be used as a principal residence or a vacation home for longer than 14 days in a given year.

To make this as simple as possible, think of like-kind property as what the intended use is from an investment mindset versus the intended use from a practical sense. A single-family home that is rented to produce income and appreciation is not similar in a practical sense to a farm that is producing income from selling crops.

However, to the IRS, they are “like-kind” since their intended use is the same. They are to be used as investments.

Below is a short list of properties that can and cannot qualify as “like-kind” in a 1031 exchange.

List of Like-Kind Properties

| Property Type | Like-Kind |

|---|---|

| Short-term Rental | |

| Long-term Rental Property | |

| Speculative Land | |

| Second Home | |

| Timeshare | |

| Apartment Building | |

| Trailer Park | |

| Commercial Building | |

| Land for Growing Crops | |

| Delaware Statutory Trusts (DST) | |

| Office Condo | |

| Principal Residence | |

| Home for Family Member | |

| Property(s) Outside the United States |

How Much Does a 1031 Exchange Cost?

The cost for a typical 1031 exchange can range from $500 to $1,200. The main expense is paid to the qualified intermediary for preparing the required documentation and holding the proceeds from the sale until the exchange is completed.

Can You 1031 Exchange a Primary Residence?

A 1031 exchange is used to defer the capital gains taxes on investments only. Principal residences, second homes, and timeshares are not considered investment properties to the IRS.

What Is a DST?

A Delaware Statutory Trust (DST) is a fractional ownership in larger investment properties, such as medical offices, industrial properties, or multifamily apartments. A DST provides more options for investors who don’t want to manage properties or desire more diversification.

Finding eligible DST properties is also less time-consuming because investors are exchanging into existing investments that are already under management.

What Are the Disadvantages of a 1031 Exchange?

- Additional paperwork, regulations, and fees

- Meeting the 45-day rule

- Closing in 180 days

- Replacing the value of the Relinquished Property

- Replacing the debt load of the Relinquished Property

- The risk of greater tax liability if the capital gains tax rate increases in the future

- Deterrent to some property buyers who may not want the added complexity impacting their transaction

Do You Ever Have to Pay Taxes on a 1031 Exchange?

Yes, a 1031 exchange is a way to defer taxes to another day in the future. Always advise your clients to speak to a CPA to discuss the benefits and risks of a 1031 exchange.

How Long Must You Hold a Property After a 1031 Exchange?

To avoid a tax penalty for not purchasing a “like-kind” investment, you must hold the property and use it for the same purpose for two years after the purchase date.

How Soon Can You Move Into a Property After a 1031 Exchange?

The IRS is very clear that any property that is purchased as an investment may not be used as a principal residence for a minimum of two years. For properties purchased as short-term or vacation rentals, the exchanger may not use the property for personal use for more than 14 days each year.

Additionally, it is advised that if the intention is to move into the property and make it the exchanger’s primary residence (after two years), then the property should be held for a minimum of five years before reselling it.

What Does a Qualified Intermediary Do?

The Qualified Intermediary holds the exchange funds in a separate bank account for the benefit of the exchanger until the funds are used to purchase the exchanger’s Replacement Property.

The Qualified Intermediary also prepares the documentation for the 1031 exchange. This includes the Exchange Agreement, Assignments of Purchase and Sale Agreements, Notices of Assignment to both the buyer and seller, the Replacement Property Identification Notice, and lastly, all the accounting and tax forms.

Who Can Be a Qualified Intermediary?

While the IRS doesn’t require a person to have a license or certification to be a Qualified Intermediary, it does have specific exclusions for any person(s) who may have a conflict of interest with the parties in the exchange.

Any person who has acted as an employee, attorney, accountant, investment banker, investment broker, or real estate agent within the two-year period preceding the date of the sale of the relinquished property is treated as an agent of the Exchanger and is specifically disqualified from being a Qualified Intermediary.

Additionally, children, parents, and siblings are also disqualified as Qualified Intermediaries.

Why Are Unused Proceeds Called ‘Boot’?

The 1031 exchange originated hundreds of years ago when property owners bartered for property. Farmers would trade land for land and livestock or an ox or money. These additional items of value were known as Boot.

The 1031 exchange in the United States originated in 1921 as the first like-kind exchange authorized as part of The Revenue Act of 1921, when the United States Congress created Section 202(c) of the Internal Revenue Code.

Today, cash received or mortgage debt not replaced in an exchange is known as equity or mortgage boot.

Can You Use 1031 Proceeds to Make Repairs to Replacement Property?

The simple answer is no. Any repairs to the Replacement Property must be paid from additional funds or loans. In some circumstances, 1031 Improvement Exchanges do allow for repair, but they require much more planning and expertise than a typical 1031 exchange.

Can 1031 Exchange Proceeds Be Used to Pay Fees?

The IRS only allows fees that are required to purchase the Replacement Property to be paid from the proceeds from the Relinquished Property. These fees include title fees, real estate taxes, property insurance, and escrow fees.

However, property inspections, appraisals, surveys, and loan origination fees are NOT considered required and must be paid out of pocket in a 1031 exchange transaction.

Bottom Line

If you want to work with real estate investors, then you must know the in’s and out’s of 1031 exchanges. As real estate properties continue to rise in price, 1031 exchanges are going to become more common. Investors will need agents who can guide them through a successful 1031 exchange process.

Tell us about you so we know what to send.

Add comment