Purchasing a new home, especially for first-time buyers, is overwhelming and a bit scary. So when you finally get those buyers onboard, they will need some hand-holding. That’s where you come in! You show your amazing buyer’s agent skills, compassion, and professionalism in this pivotal moment. Your buyers need you now more than ever. Guide them confidently through the home buying journey using this step-by-step home buying checklist and the accompanying PDF download.

Download Our Home Buyer Checklist PDF

Key Takeaways

- Use the home buying process checklist as a roadmap to guide your clients, showing off your expertise as a valued, trusted advisor.

- Educate your clients on the importance of working with a skilled buyer’s agent and provide resources to help them make informed decisions at each stage of the journey.

- Communicate proactively with all parties involved, promptly addressing potential issues to ensure a smooth and successful closing.

- Empower your clients to make confident decisions by providing market insights, data, and guidance on crafting competitive offers and negotiating like a pro.

- Cultivate long-term relationships by offering ongoing support, resources, and personalized touch, demonstrating your commitment to their success beyond the closing table.

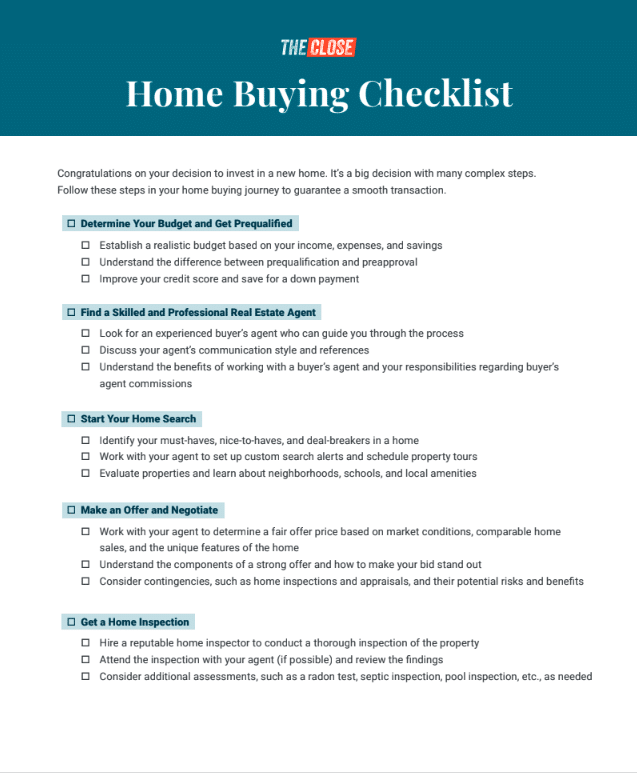

Step 1: Help Buyers Determine Budget & Get a Loan Prequalification

Encourage them to work with a lender early to improve their credit and save for a down payment.

Step 2: Be the Skilled Real Estate Agent Clients Need

Step 3: Assist Buyers in the Home Search

Step 4: Guide Clients Through Offers & Negotiations

Step 5: Recommend Trusted Professional Home Inspectors

Step 6: Support Clients in Finalizing the Loan

Step 7: Prepare Buyers for the Final Walkthrough & Closing

Step 8: Celebrate Your Buyers’ Success & Provide Ongoing Support

📌 Pro Tip

This home buyer checklist isn’t just for your existing clients. Use this checklist with your lead nurturing email campaigns and social media marketing. Or use it as a lead magnet to attract more buyer clients.

Do’s & Don’ts for Buyers Under Contract

As a buyer’s agent, another crucial aspect of your role is educating your buyers, especially first-time home buyers, on the do’s and don’ts of the home buying process checklist after they are contracted to purchase a home. This home purchase checklist contains the most common mistakes buyers make that create messy situations leading up to closing. Sit down with your buyer clients and share these simple do’s and don’ts and the consequences to help them achieve their homeownership goals.

Don’t Buy a Car or New Furniture

It’s an exciting time to dream of living in your new home, with all new furniture, and driving that new car. But until the lender has fully vetted your finances, making big purchases can disrupt your debt-to-income ratio (DTI) and boot you out of qualifying for your home loan. Wait until you close on your home to go shopping.

Don’t Make Large Cash Deposits or Move Money Around

Don’t mislead your lender when they ask about your income, other sources of income, or anything that might affect your ability to qualify for your mortgage loan. Be upfront and honest. Don’t make large cash deposits into your bank account or move finances from one account to another while the lenders still try to vet your financial stability. When in doubt, contact your lender and ask them for advice.

Don’t Apply for Credit or Increase Your Limits

When underwriting is working on verifying your income, DTI, and ability to repay the loan, they take a snapshot of your financial situation. If you apply for additional credit or increase credit limits, you’re just throwing a wrench into their process. You could throw your DTI off, which might disqualify you from the mortgage loan.

Don’t Co-sign for Anyone

It doesn’t matter if it’s your brother or sister, your aunt, your cousin, or your closest friend; don’t co-sign anything when you’re trying to qualify for a mortgage. When you co-sign anything–from a rental application to a car note–you’re putting yourself on the hook for anything that might go wrong, which could kill your dreams of home ownership in a flash. Anyone who needs your creditworthiness to get a new apartment must wait until you close on your home.

Don’t Get Behind on Your Payments

Qualifying for a home loan is no small thing, and it’s typically a longer process than many think. Now is not the time to skip a payment on your existing car note or your light bill. Those payments keep your credit score up. If you miss any of these payments, your credit score could be negatively affected quickly. So, keep those payments on time.

Don’t Change Jobs or Careers

This is a big one, especially if you’re relocating. If you don’t need to change your job, wait until you close on your new home. You may need to change jobs if you’re moving to another city, but don’t do it in the midst of buying a new home. You can count the last couple of years as income when you change jobs within the same field. But when you change to a new career, you’re starting over. None of your previous income counts toward your new career, which could hurt your chances of getting that house.

Don’t Change Banks

Don’t change banks in the middle of qualifying for a loan. Your lenders don’t want to search for your money after they start working on your loan. If you don’t like your current bank, wait until after you’ve closed on your home to migrate to a different one.

Don’t Close Credit Cards or Max Them Out

Believe it or not, closing a credit card can negatively impact your credit score. In essence, you’re losing some of your credit ceiling when you close a credit card, which, in turn, upsets your DTI ratio. For the same reason, don’t overuse your credit cards. Keep your credit usage to a maximum of 30% of your credit limit, and try to pay it off each month. Anything that negatively impacts your credit score could cost you your dream home.

Do Save Enough Money for Closing

Make sure you save enough money for closing costs in addition to your down payment. A good amount to save is around 10% of the home’s purchase price. You should get the final amount needed for the closing the week prior. Set that money aside and don’t spend it.

Do Be Cautious When Consolidating Debt

When you start working with a lender, they will coach you to get into a better position to qualify for a mortgage. But don’t go outside of their advice. Ask your lender about debt consolidation before you do anything with an outside company. Sometimes, consolidating can affect your credit score negatively, and that could set your timeline back by months.

Do Wait Until You’re Fully Funded Before Making Big Financial Changes

Wait until you have signed the papers on your new home and it is fully funded, meaning all the closing documents have been signed, the money has been received from the lender and transferred to the buyer, and you receive keys to the property, before making any significant changes in your finances. Disrupting your finances before your loan closes could disqualify you from the loan, and you won’t be able to close on your new home.

Do Hire a Skilled & Professional Real Estate Agent

I know you probably have a cousin or aunt who used to be a real estate agent, but you need someone who will work for you and protect your interests and knows the current local market. For most home buyers, this is the single largest investment, and you want someone who knows the market, is a skilled negotiator, and will work with you to help you achieve your homeownership dreams.

Your Take

As real estate agents, we aim to help our clients achieve their homeownership dreams while ensuring a smooth and successful transaction. By using this comprehensive home buying checklist (click this link to jump back to the top of the article if you forgot to download it!) and sharing these do’s and don’ts, you’ll be well-equipped to guide them through the process confidently. Remember, you are their trusted partner, so be ready to offer your expertise, answer their questions, and celebrate their successes.

Have your buyers messed up their transactions? I’ve seen my fair share of deal-killing mistakes. I could help them work through some, but others were out of my control. But those unfortunate stories have become invaluable for getting my point across to buyers. I would love to read some of your best stories in the comments!

Tell us about you so we know what to send.